By Chris Bruen

Chris Bruen is Senior Director of Research and Chief Economist, with primary responsibility for aiding in and expanding upon NMHC’s research in housing and economics. Chris holds a bachelor’s degree in Finance from The George Washington University and an M.S. in Economics from Johns Hopkins University.

Interest rates and market swings have reshaped short-term returns, but long-term apartment investments continue to outperform other commercial asset classes, while supporting the operation and expansion of the nation’s housing supply.

Capital investment plays an essential role in ensuring that the apartment sector, a major component of the U.S. housing system, can develop, operate and preserve housing for more than 40 million Americans across a wide range of income levels, markets, and property types. A 2018 NMHC Research Foundation study conducted by Mark J. Eppli, Ph.D. and Charles C. Tu, Ph.D. found that privately held apartments generated higher returns compared to other types of commercial real estate (retail, industrial and office) from 1987 to 2016, both on a nominal and risk-adjusted basis and for a range of holding periods.

More than eight years have now passed since this study was released—during which time the real estate market has experienced significant volatility from (in chronological order) the COVID-19 pandemic and corresponding recession, aggressive fiscal and monetary stimulus, elevated inflation and rapid interest rate hikes—so we wanted to examine whether our more up-to-date dataset (1987-2026) showed a change in risk-adjusted apartment returns. Strong risk-adjusted returns matter beyond the balance sheet. When apartment investment is financially viable over the long term, it signals to the market that rental housing production is worth pursuing (instead of other asset types), supporting the kind of private-sector activity that the nation needs to close its housing affordability gap.

While we did record a downward revision for short, one-year holding periods, more recent data actually show risk-adjusted, ex-post apartment returns associated with longer-term, 3-, 5-, 7-, 10-, and 15-year holding periods increased and were comparatively unaffected by these shorter-term market fluctuations.

Furthermore, our more up-to-date dataset continues to show apartments outperforming all other real estate types (retail, industrial, office and hotel) on a risk-adjusted basis.

Longer Holding Periods Continue to Produce Stronger Risk-Adjusted Apartment Returns

The private apartment market returned an average of 4.8% per year from 4Q 2016 to 1Q 2026 (nominal, unlevered), according to data from NCREIF, lower than the 8.9% average observed during the preceding three decades (1Q 1987 to 4Q 2016). Yet, one reason that apartment returns were so much higher during the earlier part of this data series (the late 1980s through the early 2000s) is that interest rates were also much higher. Because Treasury Bills provide a risk-free rate of return for investors, apartments or any other “risky” asset must offer returns that are expected to be higher than this risk-free rate in order to attract investment capital.

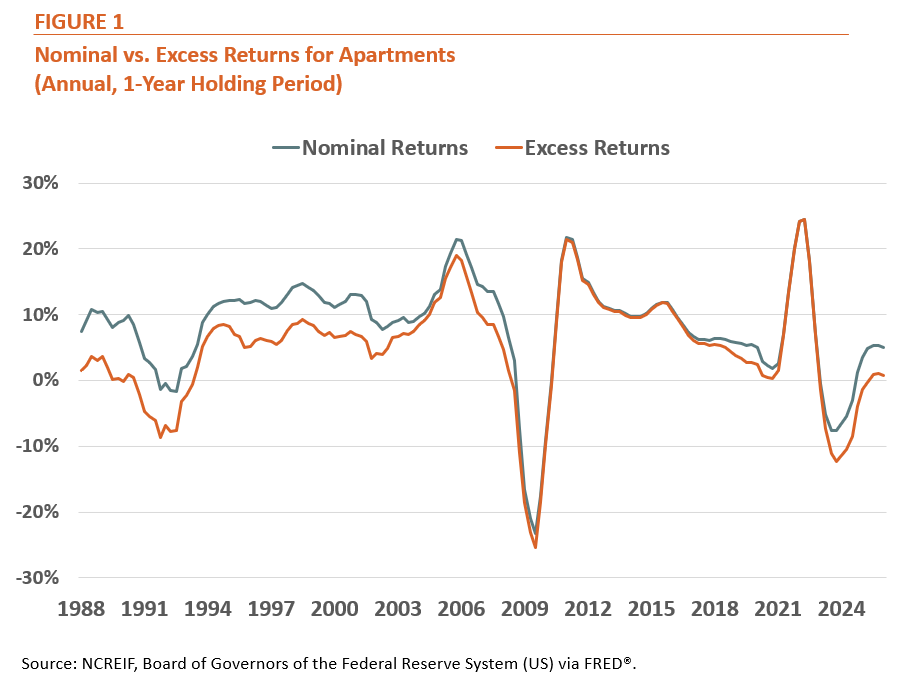

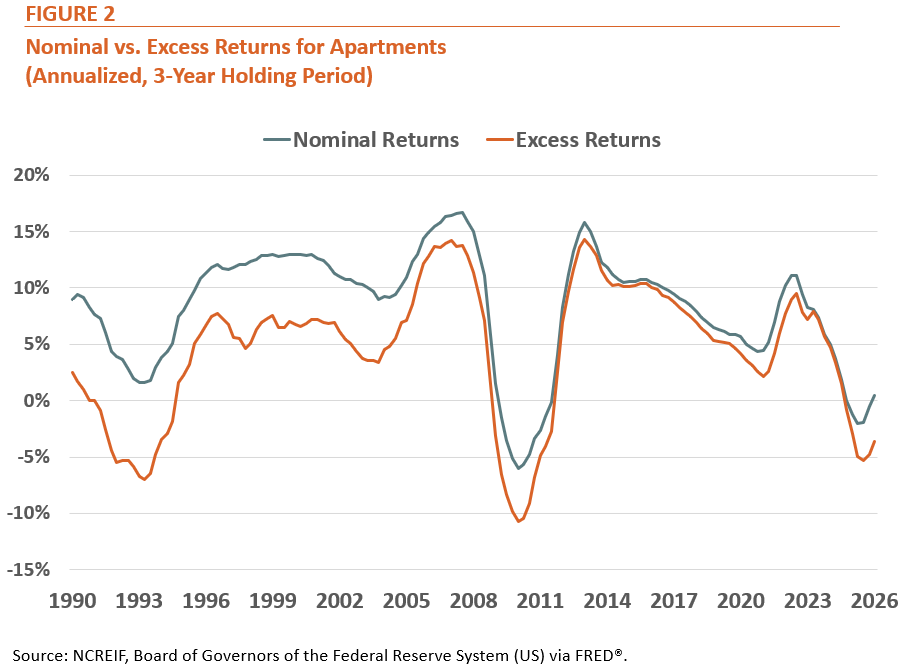

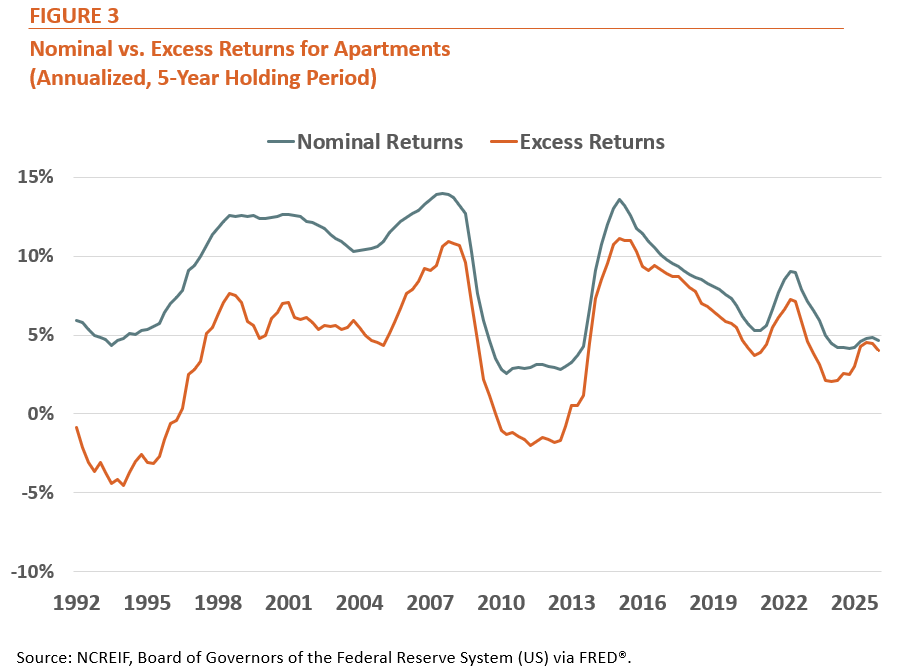

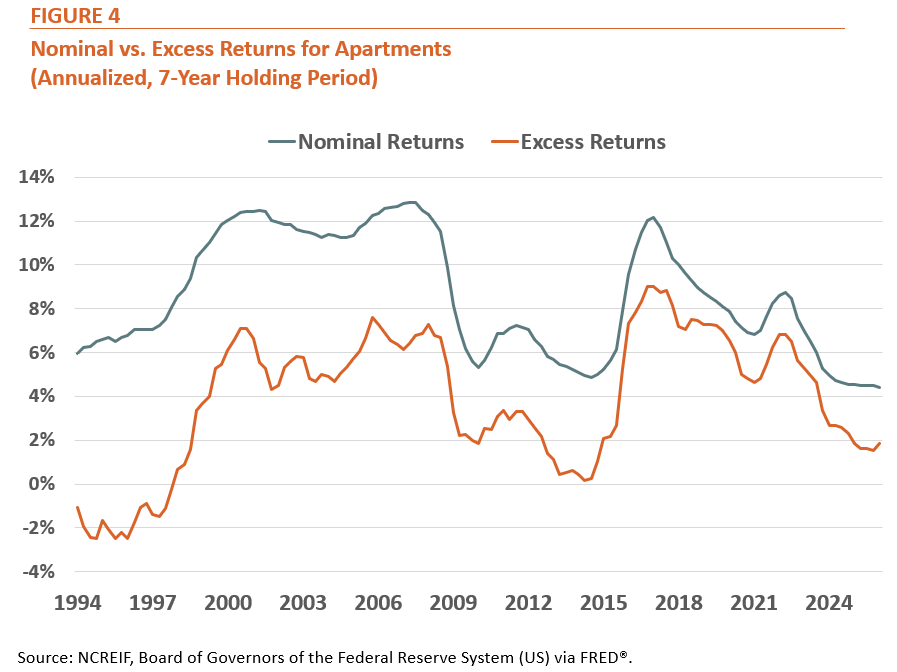

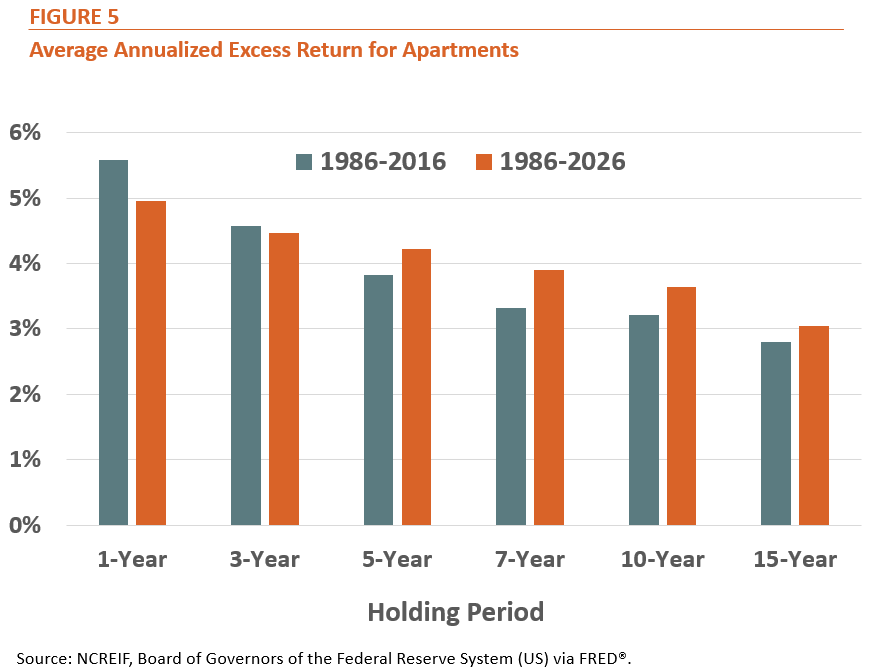

Figures 1 through 4 below illustrate how the gap between nominal and excess apartment returns has narrowed over time as interest rates have decreased.

|

|

|

|

When we updated our dataset from 2016 to 2026, the average excess returns associated with 1- and 3-year holding periods became slightly lower, but those with 5-, 7-, 10, and 15-year holding periods became slightly higher.

|

|

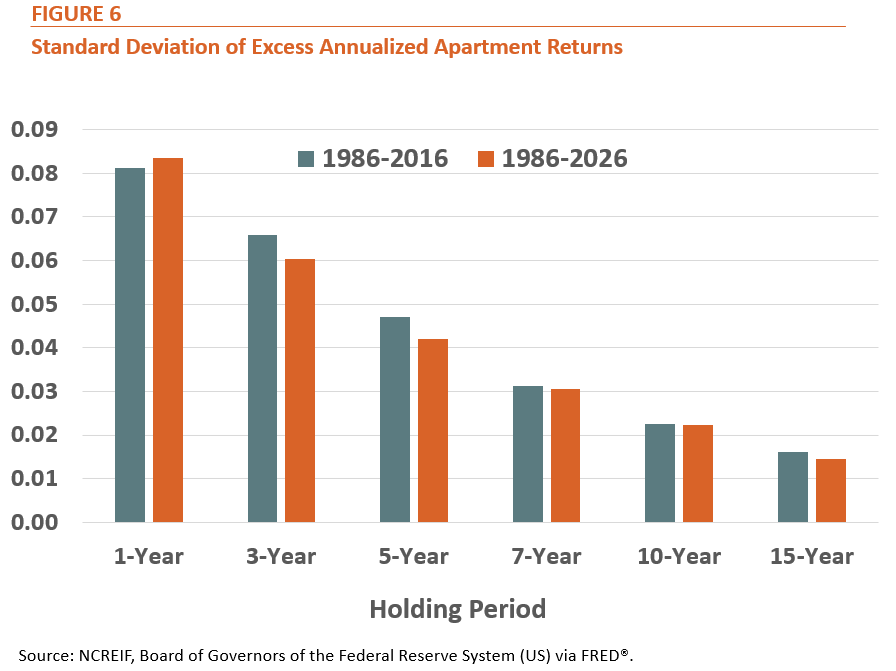

Apartment returns associated with shorter holding periods have also experienced considerable volatility since the end of 2016. One-year holding period returns ranged from -7.6% (for investments purchased in 3Q 2022 and sold in 2023) to +24.5% (for investments purchased in 2Q 2021). But these short-term market swings are far less impactful for longer-term investors. In fact, we found that the standard deviation of excess returns (a common measure of market volatility) actually became lower for 3-, 5-, 7-, 10-, and 15-year holding periods when we updated our data from 2016 to 2026.

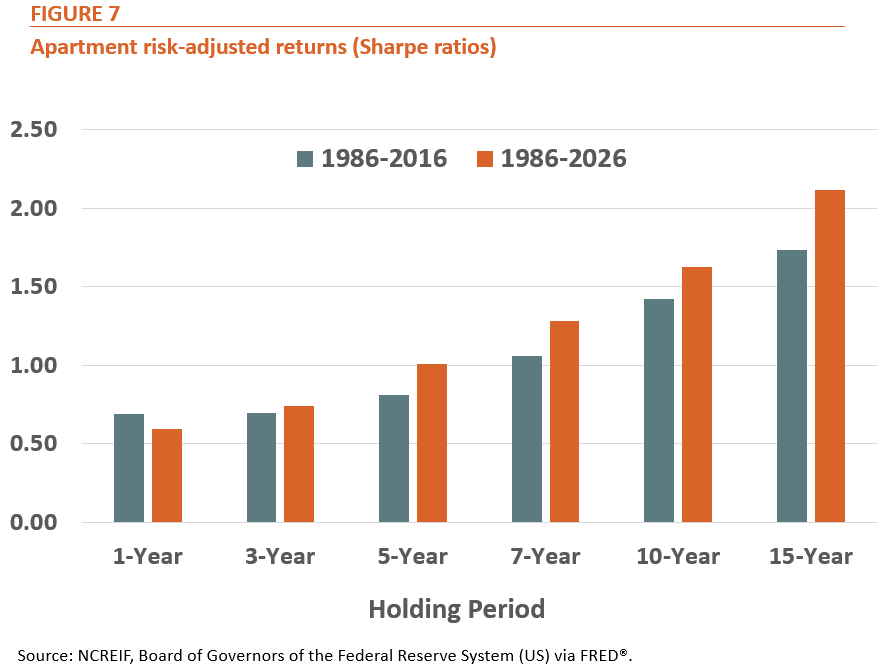

The net effect of this increase in excess returns and decrease in volatility across longer holding periods was an increase in risk-adjusted returns, measured by the Sharpe ratios illustrated above.1 Taken together, these findings suggest the performance of apartment investments is heavily influenced by holding period length and reinforce the importance of long-term investment horizons.

Apartments continued to outperform other real estate types on a risk-adjusted basis

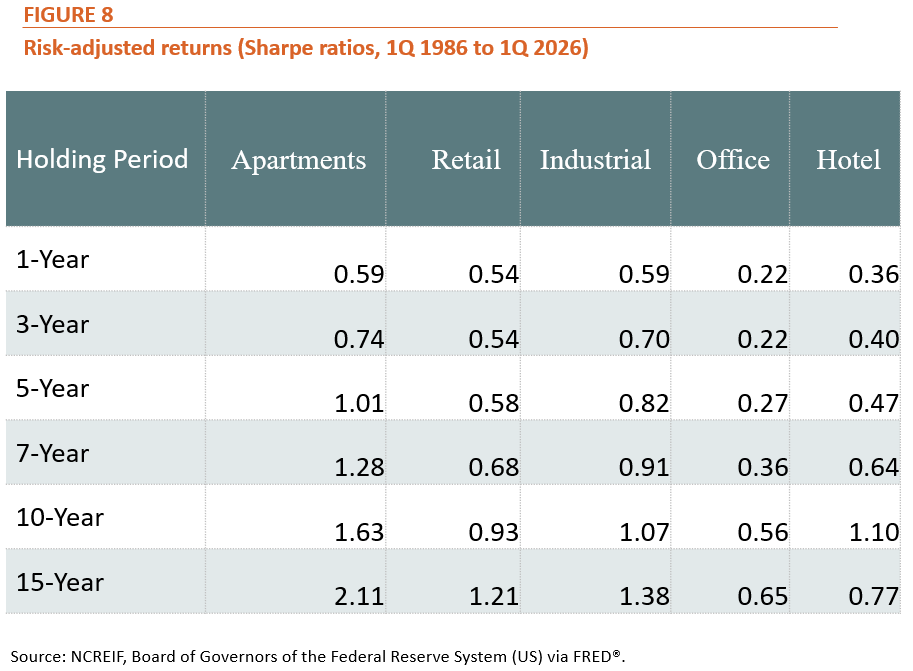

Looking at the entire updated NCREIF dataset from 1Q 1987 to 1Q 2026, apartments recorded the highest risk-adjusted returns of all commercial real estate types for all holding periods (apartments and industrial were tied for 1-year holding periods when rounded), followed by industrial, retail, hotel and office properties.

Still, as with all investments, past performance does not guarantee future returns, and current market conditions present many challenges to prospective investors. For instance, historic levels of new supply in some markets, coupled with slowing job growth, has yielded lower-to-negative rent growth in recent years. In addition, persistent inflationary pressure continues to keep interest rates elevated, and operating costs continue to rise.

The updated findings suggest that apartments have continued to demonstrate comparatively strong long-term risk-adjusted performance relative to other major commercial real estate sectors, particularly across longer holding periods where volatility has historically been lower and excess returns more stable. From a broader market perspective, sustained capital allocation to the apartment sector plays an important role in supporting the ongoing operation, rehabilitation, and expansion of the nation’s rental housing stock.

1 Calculated as the average excess apartment return—the nominal return minus a “risk-free” interest rate (measured by historical treasury rates)—divided by the standard deviation of excess returns to account for risk.

Questions or comments on Research Notes should be directed to Chris Bruen, NMHC Sr. Director of Research and Chief Economist.