By Chris Bruen

Chris Bruen is Senior Director of Research and Chief Economist, with primary responsibility for aiding in and expanding upon NMHC’s research in housing and economics. Chris holds a bachelor’s degree in Finance from The George Washington University and an M.S. in Economics from Johns Hopkins University.

Policymakers, advocates and researchers have increasingly questioned what the presence of large investors means for renters and housing affordability. There are a variety of terms that have begun to be used, somewhat interchangeably, including “corporate landlord” and “institutional investor”. While definitions may differ, they all can obscure the same underlying question: Does the type of ownership entity meaningfully affect rents, housing supply or long-term affordability? Relatively little empirical research has been conducted on this topic to date, despite media reports to the contrary. This Research Notes examines what we will refer to as “professional housing providers”—private owners other than individual investors—and how their market share and influence vary by product type and geography.

Individual Investors Less Prevalent Among Larger Rental Properties

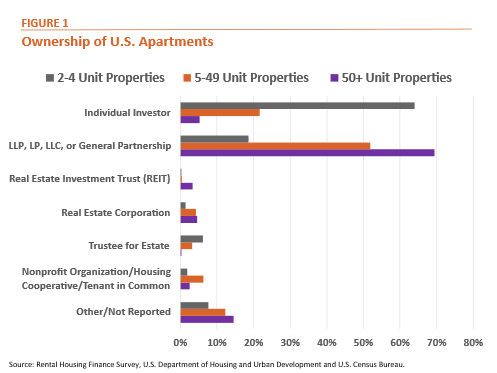

According to HUD’s Rental Housing Finance Survey (RHFS), individual investors in 2024 owned 58.8% of rental homes in 2–4-unit properties, 19.2% of homes in 5-24-unit properties, 5.7% of homes in 25-49-unit properties and just 4.6% of homes in properties with 50 or more units (it makes sense that few individuals would possess the capital necessary to develop or purchase an entire 50+-unit apartment property). We can infer, then, that professional housing providers own a much higher share of larger multifamily properties.

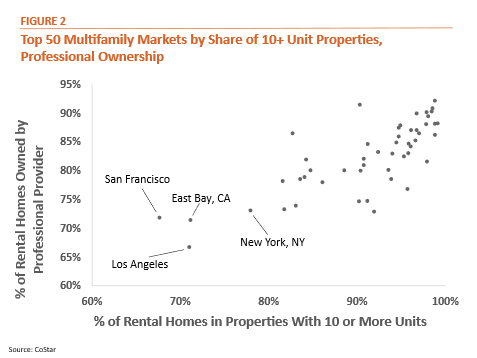

For this reason, multifamily markets with larger property sizes tend to have a higher share of professional ownership. For instance, Figure 2 below shows that San Francisco, East Bay, Los Angeles and New York—markets with the lowest share of larger, 10+-unit properties among CoStar’s top 50 markets—also have some of the lowest shares of professional housing providers.

Multifamily markets with the lowest share of professional housing providers also appear to be in more expensive, supply-constrained coastal areas with more stringent regulations around development. According to the Wharton Residential Land Use Regulatory Index, the San Francisco metro area, which includes both the San Francisco and East Bay CoStar markets, is the most regulated housing market in the country in terms of local land use restrictions, followed by New York, Providence, RI (not one of CoStar’s top 50 markets), Seattle and Los Angeles.

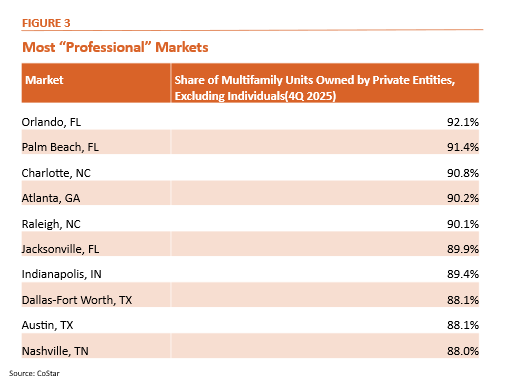

At the other end of the spectrum, the ten CoStar markets with the highest share of professional ownership are nearly all located in the South (except for Indianapolis), where there are fewer restrictions around development. Many of these markets have led the nation in multifamily construction over the past decade: Austin expanded its apartment supply by 78.3% since 4Q 2015, Nashville grew its supply by 75.8% and Charlotte grew its supply by 73.7%.

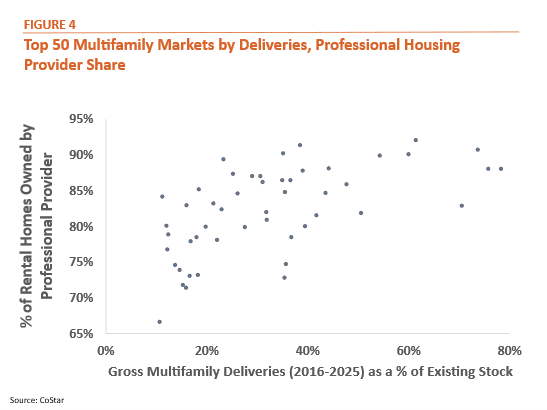

These higher levels of construction in markets that tend to have larger properties have contributed to the longer-term national trend of increasing property size among multifamily development.

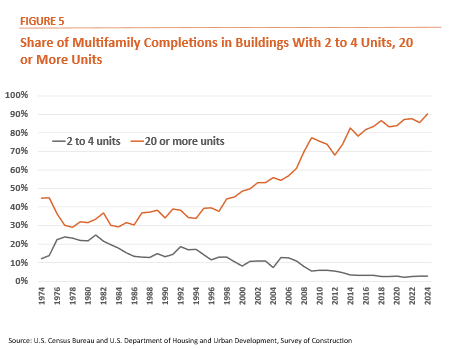

The U.S. delivered 608,000 multifamily homes in 2024, according to data from the U.S. Census Bureau, the highest amount since 1986. What is more, nearly all these new homes (90.1%) were in buildings with 20 or more units (the highest on record), whereas just 2.7% were in buildings with 2 to 4 units.

This increasing prevalence of large properties, in turn, suggests that ownership by professional housing providers has become more common over time.

Who is Building these New Units?

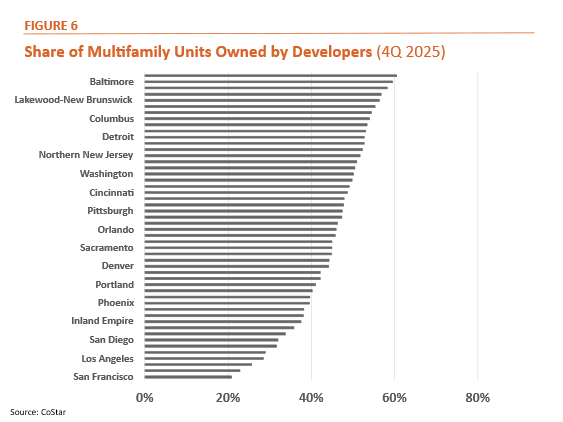

There is a very direct relationship between multifamily development and ownership; many companies—often operating with institutional capital—both develop and own apartment communities. Among CoStar’s largest 50 markets, developers owned anywhere from 20.9% (San Francisco) to 60.5% (Richmond, VA) of all multifamily homes in 4Q 2025.

What this relationship illustrates is that professional housing providers are not just entities looking to profit by buying up existing buildings; they are frequently developers as well, many of whom are responsible for the historic wave of new rental housing supply in recent years.

Conclusion

The recent expansion in apartment supply did not occur in a vacuum. Delivering new rental housing at scale requires substantial capital, development expertise and the ability to navigate complex entitlement, financing and construction environments. The very places that are the least affordable are some of the most difficult to develop, requiring the most sophistication. Data show that professional housing providers supplied the majority of capital behind this recent wave of new construction. That additional supply has coincided with a measurable easing in rent growth.

According to RealPage data, effective asking rents for professionally managed apartments declined 0.6% year over year in the fourth quarter of 2025, with rents falling in 73 of the 150 markets tracked. While many factors influence rents—including local demand conditions, wage growth and broader macroeconomic trends—the timing and breadth of moderation suggest that new supply has played a meaningful role in reducing rent increases for renters.

This does not imply that ownership scale alone determines affordability outcomes—housing markets remain local, and housing costs are shaped by land costs, regulation, construction expenses and household income growth. However, the evidence underscores a consistent economic principle: when housing supply expands meaningfully, upward pressure on rents tends to ease.

As policymakers and stakeholders evaluate ownership models and market structure, it is important to ground the discussion in observable outcomes. The recent period demonstrates that capital capable of supporting large-scale development can materially expand supply—and expanded supply is closely associated with slower rent growth and in some markets, outright declines. Any policy conversation about ownership composition should weigh these dynamics carefully, recognizing the central role that sustained development plays in improving housing affordability over time.

Questions or comments on Research Notes should be directed to Chris Bruen, NMHC Sr. Director of Research and Chief Economist.